Introduction

In the year 1978, a series of reforms were introduced to open the Chinese economy. The highly centralised, non-market system was the cause of numerous economic disasters. Famine and economic slowdowns were the disturbing reality of China during the 1960s. In a shift, the open-door policy of 1978 created hubs for foreign investment including SEZs, economic and technology development zones, and open border cities. These reforms set the foundation for the dragon to prepare its wings and set out for the sky. China, presently, is an upper-middle-class economy with high growth based on investment, low-cost manufacturing and admirable growth in industrial development. It is a growing influence in Asia through trade, investment & and ideas. However, the COVID-19 pandemic became a roadblock in its rise to the top, resulting in a spiraling structural slowdown of its economy, which the Chinese have yet to be able to recover from in 2023. With an increase in debt, consumer demand down, sluggish exports and domestic sectors taking the hit, the rise and slowdown of the dragon need to be read into.

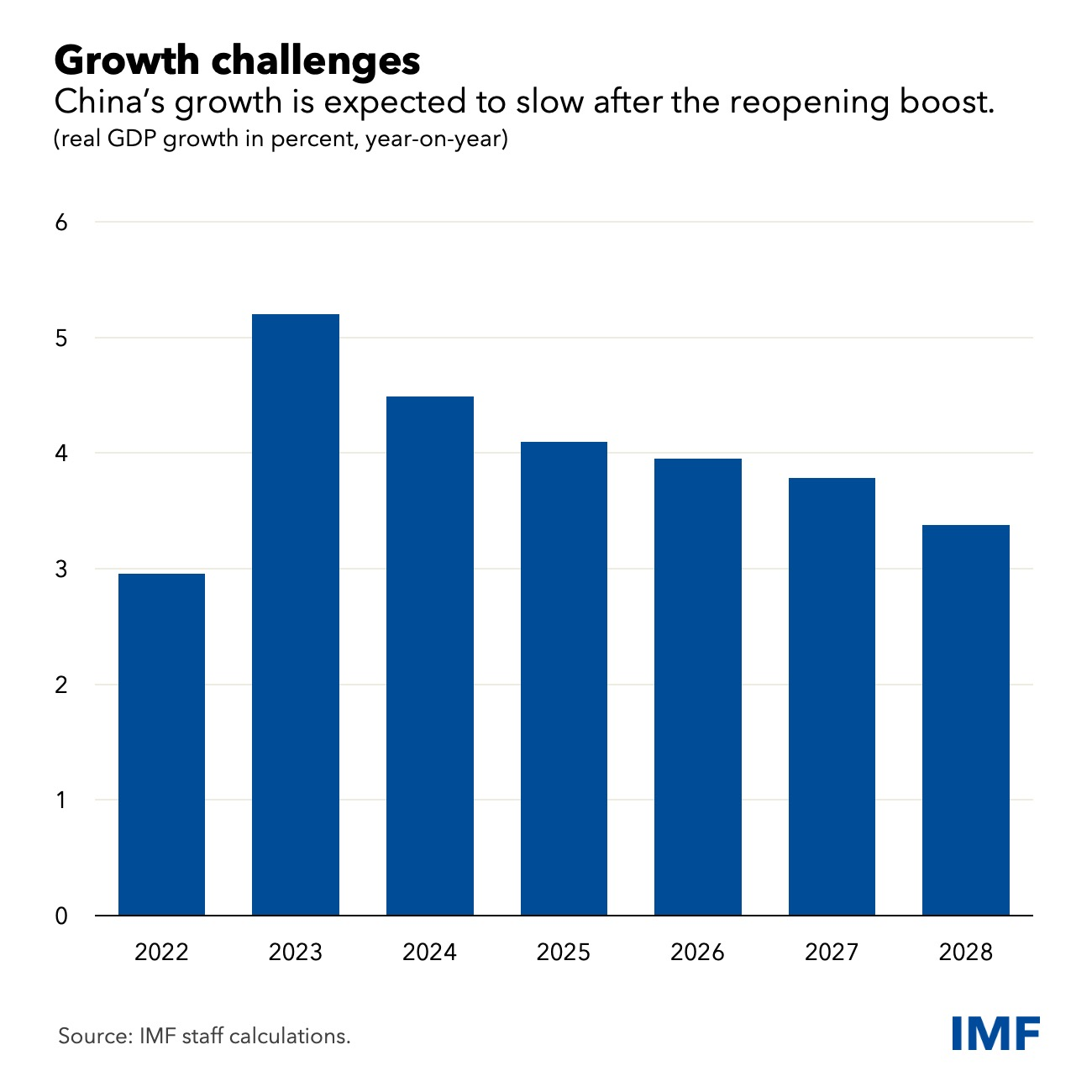

The above graph shows the updated forecast by the IMF for China’s GDP growth from 2022 to 2028. The Chinese economy was projected to grow 5.4 % in 2023. But growth is expected to slow down in 2024 to 4.6 %. The subsequent years reflect further downshift in GDP growth due to weakness in property sector and diminishing external demand.

The Chinese government is on its toes, trying to fix the crisis and ensure that it is not here to stay. But before reading into the counter-reforms, a detailed understanding of the causes is required. Most of the reasons for China’s decline in the economy predate the pandemic, however, the complete lockdown coupled with the global economic crisis added grease to an already slippery slope.

A Slip in Consumer Spending

Consumer spending has lagged China’s overall economic growth since the pandemic started in early 2020. The country ended its stringent COVID-19 restrictions in late 2022, but the economy’s initial recovery has slowed amid a real estate market decline and a drop in exports. However, household consumption has always been the lowest in China even before COVID.

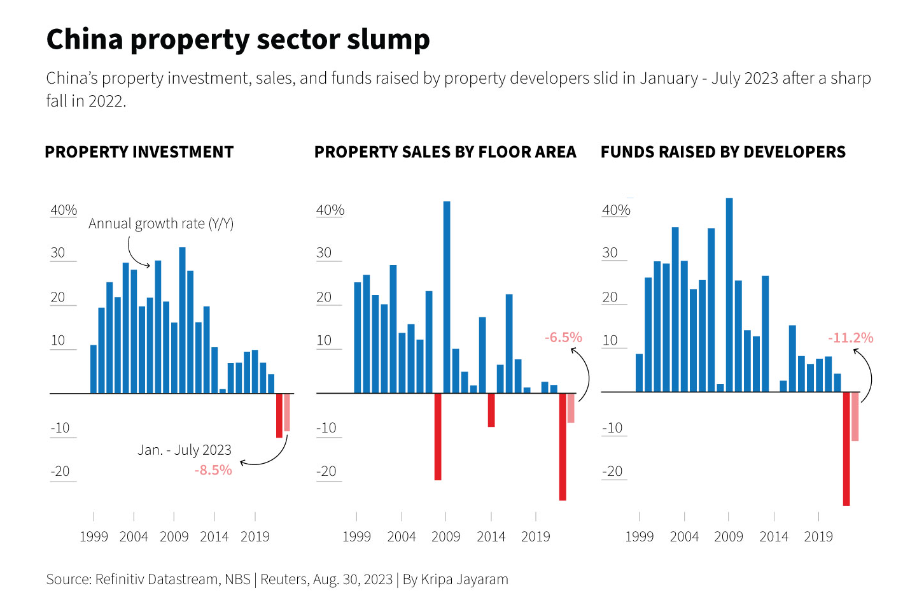

This graph shows the performance of the property sector of China. The pink bar reflects the negative performance across investment, sales and funds raised in the sector. Investment plummeted by -8.5%, while sales showed a negative performance of -6.5 %. Developers faced a downfall in funds by -11.2 %.

What is different now is that it has targeted China’s property sector, which held much of the household wealth. Property and related industries have often contributed highly to the GDP. However, since the beginning of the pandemic, more than half of the biggest property developers in China have gone into default.

Lenders reduced interest rates that cover half of the country’s mortgage loans in September. Some major second and third-tier city authorities lifted all restrictions on housing purchases from July. Analysts argue that many of Beijing’s policy measures towards property have been well-intentioned but ineffective — trying to strike too delicate a balance between offering enough liquidity support and not spurring further speculation in the sector.

China’s Local Debt Problem

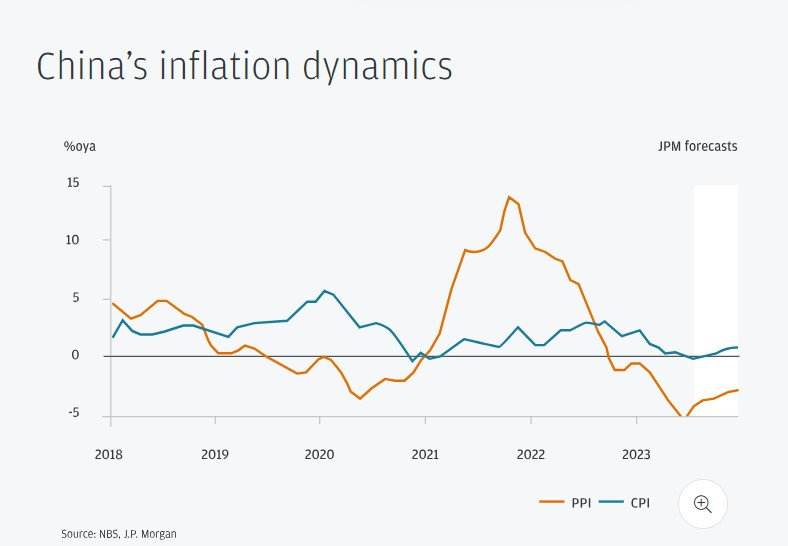

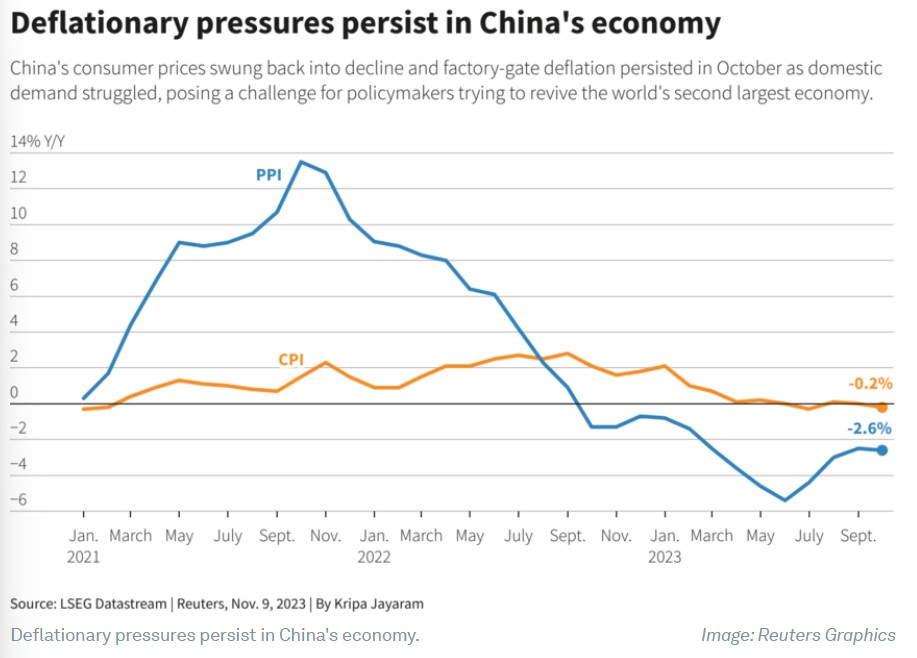

Producer Price Index (PPI) measures the average change in sale prices of goods and services while the consumer price index (CPI) measures the average change in price of consumer goods and services. As can be inferred from the graph, China’s PPI slipped into negative after peaking in 2021. The CPI began to touch the negative territory as well in 2023.

All the public infrastructure built in China over the past decade has been financed by LGFVs-Local government financing vehicles. LGFVs borrow money from banks to build infrastructure. Though, LGFVs as investment companies have managed to transform the urban landscape of China by building roads, highways and buildings, they have not been successful in making money since most of the infrastructure built is either free or very cheap. With not generating enough money to pay back their debts, China’s provinces’ enormous amount of borrowing has become a major concern for its economy.

Local governments, typically sustained by funding from Beijing and the profits from land sales, have long been encouraged to borrow money to fund regional development. However, local government finances collapsed during the coronavirus pandemic, in part because of a surge in Covid-related public spending and a drop in land sales on which they relied for revenue. With a massive pile of onshore debt repayments due in 2023 and 2024, the stress on local governments, already struggling during an economic slowdown, has intensified. The impact of the debt crisis has been apparent in the services being provided by the local governments as well with some provinces complaining of lack of public services.

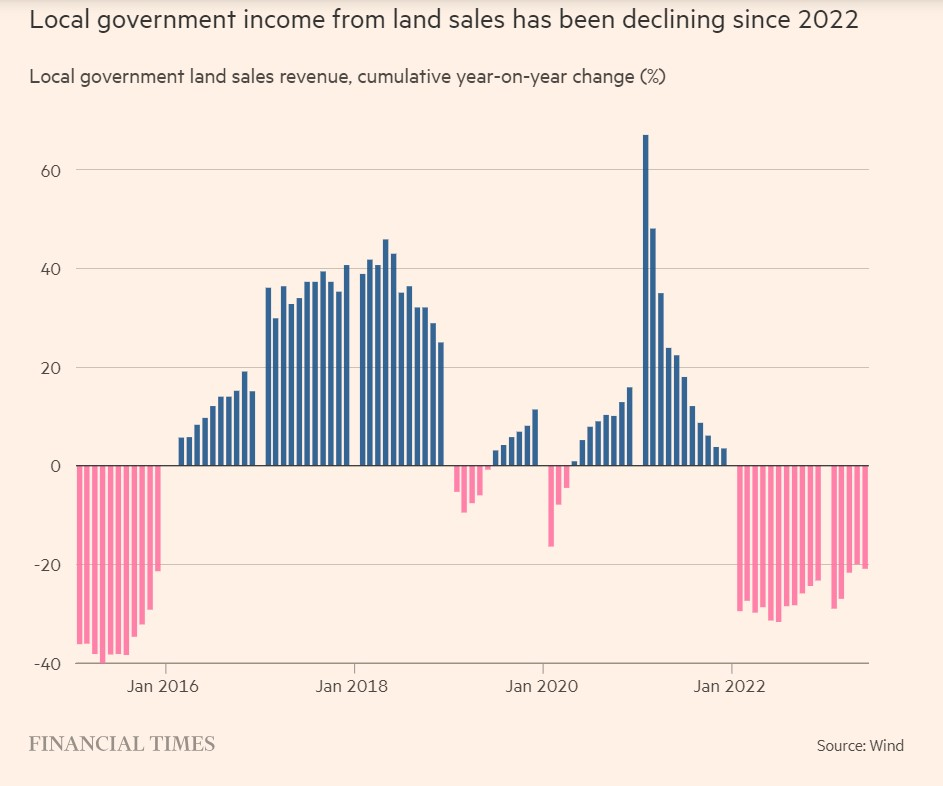

Local government’s income from land sales has been on decline since January 2022.

A Sharp Fall in Exports

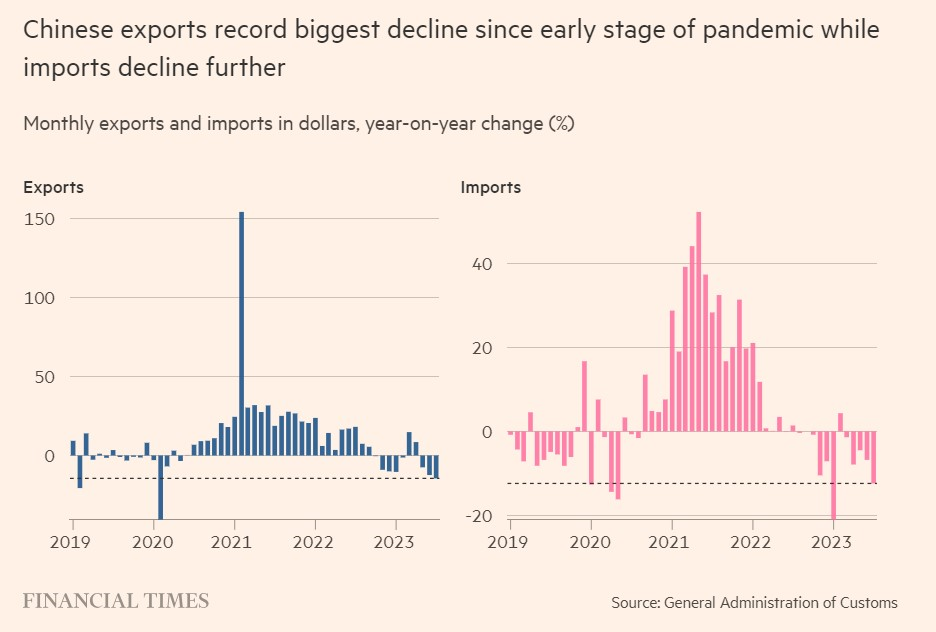

Reports in August stated that Chinese exports and imports fell sharply in July, adding to the concerns about the growth of the world’s second-largest economy. Exports declined by 14.5 % YoY, the lowest they have been since the start of the pandemic in 2020. Weakness in international trade along with contraction in manufacturing activity are regarded as some of the many causes of such sluggish performance. China’s exports in the past three years have provided a big push for its economic growth. China’s exports experienced growth after a significant pushback in 2020 however, imports grew at a higher rate leading to a trade deficit. In 2023, exports recovered slowly but imports came down significantly reflecting a slight trade surplus.

The graph shows China’s monthly exports and imports from 2019 till October 2023. Exports from China saw a positive run starting in 2021, despite the impact of COVID-19, while imports increased simultaneuoly till beginning of 2023 before dropping significantly.

Deflation in China

Due to the low consumer confidence and mounting debt, reports of China slipping into deflation started to gain stage. Consumer prices fell 0.3% YoY in July. Grace Ng, the senior economist at JP Morgan, related the deflation risk in China to the decline in the global commodity cycle. Government policies have been inclined towards production and investment instead of consumption. Households are more cautious with their spending given the country’s economic state. Food prices in China declined -1.7% while producer goods prices PPI fell -3.7% and consumer goods PPI fell -0.2%.

Deflationary pressures persist in China’s economy with consumer prices back into decline and sales of businesses lowered even further.

Government Response

Chinese economic slowdown has impacted all major sectors from property to stocks and global exports. The government has stepped up stimulus in recent months, trying to curtail further slowdown of the economy.

- In the property sector, the down payment ratio was reduced for first and second homes

- Lowered key interest rates

- Freed up more long-term cash into the banking system

- Support for household consumption

- Issuance of special local government bonds

Though improvement may be slow and limited, some areas have shown improvement. According to the data released by the National Bureau of Statistics, China, the GDP increased 4.9% in July-September from the year prior. Retail sales improved by 5.5% while the unemployment rate was down to 5%. Economic activity has shown some signs of stabilisation with factory activity picking up and consumption recovering. The IMF upgraded its GDP forecasts for China from 5% to 5.4% in 2023. The reason for such an upgrade is attributed to a sovereign bond issuance of $137 billion/ 1 trillion yuan to support the economy.

Sources

- https://www.reuters.com/markets/asia/why-is-chinas-economy-slowing-down-could-it-get-worse-2023-09-01/

- https://www.imf.org/en/News/Articles/2023/11/07/pr23380-imf-staff-completes-2023-article-iv-mission-to-the-peoples-republic-of-china#:~:text=The%20Chinese%20economy%20is%20projected,market%20and%20subdued%20external%20demand.

- https://www.reuters.com/breakingviews/chinas-growth-is-buried-under-great-wall-debt-2023-09-13/

- https://www.reuters.com/world/china/imf-upgrades-chinas-2023-2024-gdp-growth-forecasts-2023-11-07/

- https://www.reuters.com/markets/asia/why-is-chinas-economy-slowing-down-could-it-get-worse-2023-09-01/#:~:text=Given%20China’s%20debt%2Dfuelled%20investment,to%20tinker%20with%3A%20household%20consumption.

- https://www.ft.com/content/e8cb37b6-df30-4729-8509-8fc4d482d287

- https://www.jpmorgan.com/insights/global-research/international/china-deflation

- https://www.csis.org/analysis/experts-react-chinas-economic-slowdown-causes-and-implications

- https://www.bloomberg.com/news/articles/2023-07-11/why-china-s-economy-is-slowing-and-why-it-matters#xj4y7vzkg

- https://www.bloomberg.com/news/articles/2023-11-13/china-s-credit-growth-weaker-than-expected-in-october#xj4y7vzkg

- https://fingfx.thomsonreuters.com/gfx/rngs/CHINA-DEBT-GRAPHIC/0100315H2LG/