In this week’s newsletter, we talk about Google vs Indian apps, IPO financing, the history of free samples and a lot more.

If you’d like to receive our 3-min daily newsletter that breaks down the world of business & finance in plain English – click here.

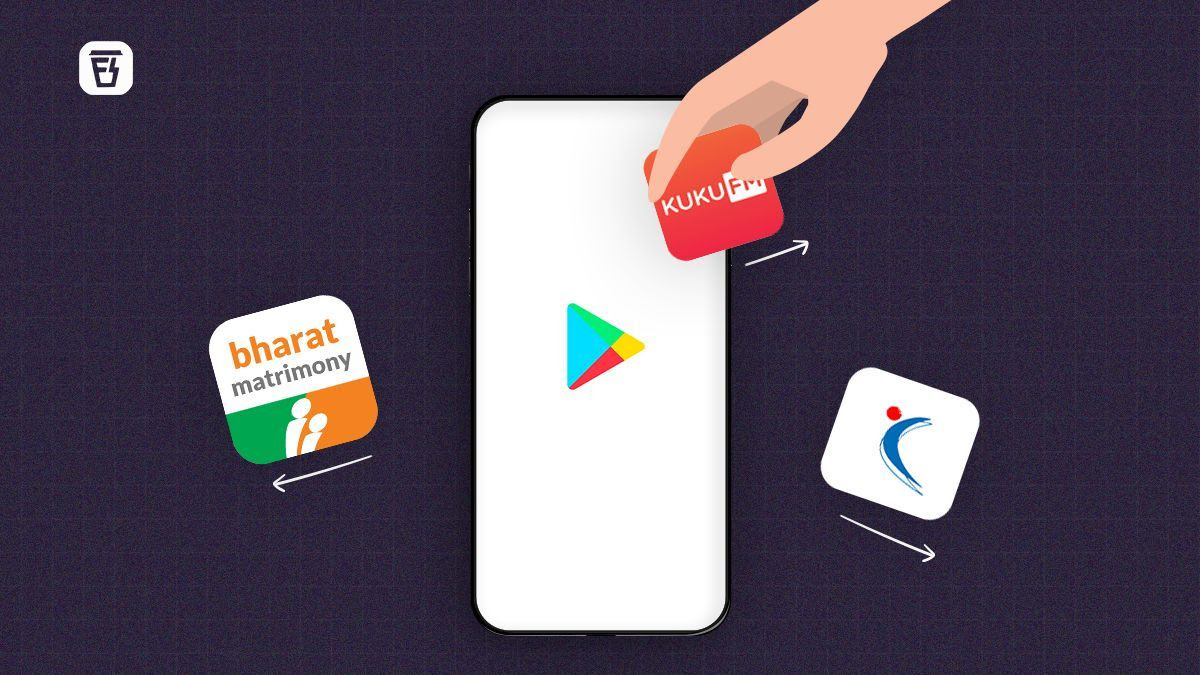

Why did Google kick Indian apps off the Play Store?

“Google is the most evil company for businesses…Today they have delisted us again…This will completely destroy our business and make Kuku FM [unaffordable] for the majority of the country, but when [has] a monopoly cared about anything beyond itself.”

Wait…what’s going on?

Well, that’s what the co-founder of Kuku FM posted on LinkedIn on Friday. And he said that because Google chucked his app out of the Play Store! So if you searched for the app you would get a message saying “This app isn’t available” (as of Saturday evening).*

For the uninitiated, Kuku FM is a 6-year-old audio platform that hosts books and podcasts across 7 languages. Anything that’s not music.

But what is relevant to our discussion is that Kuku FM has over a whopping 10 million downloads on the Google Play Store!!!

Now we’re going to make an assumption here. CapTable says that 11% of people who download the app convert into paying subscribers. We don’t know if that number is specific to people who download it from Google Play Store, Apple Store, or even via Kuku FM’s own website. But let’s say it’s an average. So that means Kuku FM likely has around 1.1 million customers who download the app on Google’s Play Store and pay around ₹899 a year for the subscription.

Okay. But why does that matter?

Well, for that we need to understand how Google’s Play store operates.

See, over 95% of smartphones in India run on Android. That’s Google’s operating system. So whether it is a Samsung or a Motorola or an Oppo, it doesn’t matter — they all use Android.

And the thing is because Google owns Android, they have leverage. They simply have to pay a visit to the phone manufacturer and tell them, “Hey, if you want to use Android, then you better preload our suite of apps — the Play Store, Google Maps, YouTube, Chrome…” And voila, these apps end up being preinstalled when you buy a new phone.

So if you want to download an app, you’ll end up clicking on the Play Store more often than not.

But that also means that Google pretty much operates a monopoly. And monopolies are quite detrimental to the interests of consumers. They can set up arbitrary rules as per their whims and fancies — like Google demanding a 30% commission on in-app payments. Or mandating that apps use only Google’s internal billing system.

And in economics, that practice is often called a ‘monopoly rent’.

Think of this as the money that a business makes by virtue of not having efficient competition. It’s the money it makes just because it has the power to charge more. Or it’s money that it makes without creating any further value but by just existing.

To sum up, Google built an operating system that became dominant -> It used that to sweeten its pot by striking deals to promote its own suite of apps -> And it made monopoly rent by controlling distribution.

So in the case of Kuku FM, if you assume that 1.1 million folks pay ₹899 via the app downloaded on the Play Store, Google keeps a cut that could be as high as ₹270. Put together, it’s worth tens of crores of rupees!

And Google calls it a ‘Service Fee’ for giving apps access to its massive Android userbase. That’s their position. And they also contest that they are not monopolistic. Samsung has its own app store. So it’s not like others can’t enter the market. Even you could build one if you wanted. However, despite there being a limited barrier to entry, very few app stores have managed to command the success and influence Google’s Playstore has managed. So they’ll argue that they’re playing fair and if companies want to showcase their apps on Google’s platform they’ll have to pay.

Anyway, this monopoly rent is a big point of contention in the tech world these days. Antitrust regulators from all over the world have been clamping down on these practices. In fact, a couple of years ago, our own Competition Commission of India (CCI) concluded that Google wasn’t allowing other app stores to flourish. Its tactics meant that only the Play Store featured prominently on all Android phones. And for that and a few other reasons, the CCI slapped a ₹2,200 crore fine on Google.

But that didn’t stop Google from charging the Service Fee. Oh, not at all. They just reduced it a bit and continued with business.

And this brings us to today. Or rather, to the 1st of March.

Out of the blue, Google decided that 10 apps in India — including Shaadi.com, BharatMatrimony, Naukri, and Kuku FM — would be thrown out of the Play Store. The tech giant says that these apps had defaulted on the Service Fees.

And the complaints against Google came thick and fast.

For instance, Anupam Mittal, who runs Shaadi.com, decided to call Google the “new Digital East India Co” and said, “This #Lagaan [rent] must be stopped!” Meanwhile, the co-founder of Kuku FM thinks that the “Indian govt [should] step in and save the start-up ecosystem.”

And maybe the government has heard that. They’ve already called Google for a meeting and they’re saying things like, “India is very clear, our policy is very clear…our startups will get the protection that they need.”

While that’s good to hear, we’re not sure if the government can force Google to mend its ways. After all, no court in the world yet has said that Google should offer their massive distribution for free to the big apps. So what can the government really do?

And sure, you might want to thump your chest and say that the Indian government should create an app store of its own. But we don’t know about that. Because a few years ago the Indian government tried to revive its app store business — something called Mobile Seva. It wanted to promote atmanirbharta (self-reliance). But that idea hasn’t really set the app world on fire. It has been a bit of a dud.

So, is there any alternative?

Well, PhonePe???

Yup, the king of UPI payments launched its own app store called Indus Appstore a couple of weeks ago. And the company will do away with commissions and levy only an annual listing fee instead. But even that fee will be waived till 2025.

Could the timing have been any better?!

We don’t think so.

But that doesn’t mean success is guaranteed. Sure, PhonePe has a massive user base that it can tap into. But it also means getting people to change their behaviour. You need them to require their muscle memory and get them to click on the Indus Appstore icon instead of the Play Store icon. And that may not be easy.

The one thing that could work in its favour though — it’s available in 12 languages. And that could nudge a sizeable number of folks into using it.

But the real kicker will only come if it somehow manages to convince phone manufacturers to preinstall the Indus Appstore on the phones. That could really move the needle. Anyway, it’s anybody’s guess how all this will pan out.

An explainer on IPO financing

Imagine. The IPO market is red-hot. There’s a new company that’s going public every other day. And the share price pop on the listing day is insane. People who invest are making sacks of money.

But the desire to make even more money sets in. People aren’t happy with just sacks. They want money by the truckload. So they turn to leverage, or in simple words, they begin to borrow money to invest. They want to invest huge sums of money to maximise their absolute gains.

And they don’t typically go to a bank and ask for a personal loan. Rather, they turn to their wealth manager or a Non-Banking Financial Company (NBFC) that offers this niche service. It’s something called IPO financing.

If you want to see this in action, you just need to look at the HNI (high net worth individual) segment of popular IPOs. You’ll often see that segment getting oversubscribed by 100 times and more. And that’s usually thanks to these loans they get. For instance, in July 2021, there were a bunch of IPOs trying to raise a total of ₹18,400 crores. But people bid a gargantuan sum of ₹8.86 lakh crores! And around 98% of that money came from these IPO-linked loans!

Heck, do you remember the spat between Ashneer Grover and Kotak Wealth Management from 2021?

Well, that was due to a tussle regarding IPO financing. Or the lack of it.

Nykaa, the beauty and fashion startup, was preparing to go public. And everyone was excited. It was a profitable startup which was quite rare. And investors anticipated a huge pop on listing. Now Grover wanted Kotak to loan him a whopping ₹500 crores to take part in the IPO. And he says Kotak backed out at the last moment and he lost the opportunity to make a killing.

But wait…how do these entities even have that kind of large sums of money to lend out to these HNIs?

Well, they usually don’t have that much money just lying around. So they have to resort to borrowing the money first. They do this by issuing something called a Commercial Paper (CP). Think of this as an extremely short-term bond that they have to repay in about 7 days.

So they launch the CP, entities such as liquid mutual funds buy it, and that money then goes into financing these IPO bets for the HNI risk-takers.

And this entire exercise of IPO financing can be quite lucrative.

See, no one’s guaranteed a full allotment in an IPO. It’s a lottery. It all depends on how much people are interested in the IPO and subscribe to it. The greater the subscription, the lesser the chances of investors getting what they wanted. And while the NBFC or wealth manager pays an annualised interest of around 5% on the CP, they charge quite a hefty interest on these IPO loans — up to 20%. That’s quite a spread.

Also, it doesn’t matter whether the HNI gets an allotment or not, they will still need to pay interest on the entire amount borrowed. *

So yeah, when the IPO market booms, it’s quite a jolly time for these IPO financers.

Okay, but isn’t this a risky proposition for the NBFC, you ask? There are massive sums of money involved at the end of the day. And there’s no collateral or security involved in the loan.

Ah, so this is where the NBFC might do something else. They expect the investor to operate on their terms. This means they take a power of attorney (POA) for the demat account and the bank account of the investors. They control the whole process — right from lending money into the bank account, making the IPO application, selling the stock, pocketing the gain or taking a loss. Everything. That reduces the risk a bit.

And this finally brings us to today.

The Reserve Bank of India (RBI) has pulled up an entity that was a big fish in the IPO financing pond — JM Financial.

Why though?

Well, there seems to be a few glaring issues as per the RBI. Apparently, JM Financial doled out IPO financing against meagre margins. Meaning that it gave clients excessive leverage. Also, the RBI seems to have a problem with the POA practice since JM Financial controls the bank accounts of customers.

The RBI says that JM Financial is in violation of regulatory guidelines. And then even mentioned the dreaded G-word — governance issues.

So the regulator laid down the gauntlet and told JM Financial that it can’t indulge in IPO financing anymore amongst a bunch of other stuff.

Now we don’t know exactly what went wrong because other NBFCs also resort to a POA and meagre financing margins. But one speculation is that NBFCs like JM Financial have flouted an RBI rule.

Around the time of the Nykaa IPO, the RBI was getting worried about the massive amounts of money at play here. So they issued a diktat saying that no customer can borrow more than ₹1 crore to finance an IPO application. Gone were the days of the Ashneer Grover-type ₹500 crore loan.

But Moneycontrol says that NBFCs have ignored the rules and are lending out more. Could JM Financial have done that too?

Another rumour doing the rounds as per the Economic Times is that JM Financial has also been inflating the IPO subscription numbers.

What do we mean?

Okay, so during the IPO, entities can simply submit incorrect applications. For instance, it might mention multiple PAN card details which will eventually lead to the application being rejected. But it will still reflect as a subscription during the IPO period and can make things look rosy.

And maybe by showing HNIs the public interest in the IPO, the NBFC could even nudge the investors into relying on IPO financing to participate.

Yeah, it’s quite a dubious practice.

Now JM Financial has categorically refuted all these allegations. They claim clean corporate governance too.

But the RBI doesn’t think so. Also, maybe even the Securities and Exchange Board of India (SEBI) will have something to say about this matter. And who knows, every other NBFC involved in IPO financing will be jittery about what’s to come.

Finshots Recommends

This week’s recommendation is The Big Short

A gripping and thought-provoking film that exposes the shocking truth behind the 2008 financial crisis and the audacious individuals who predicted and profited from the impending collapse of the housing market.

Today’s Discussion  : The Unknown History of Free Samples

: The Unknown History of Free Samples

Can you imagine living in a world without free samples? No more tasting a tiny bit of your favourite mithai at Haldiram or a free shampoo in the newspaper. It would be a sad sight!

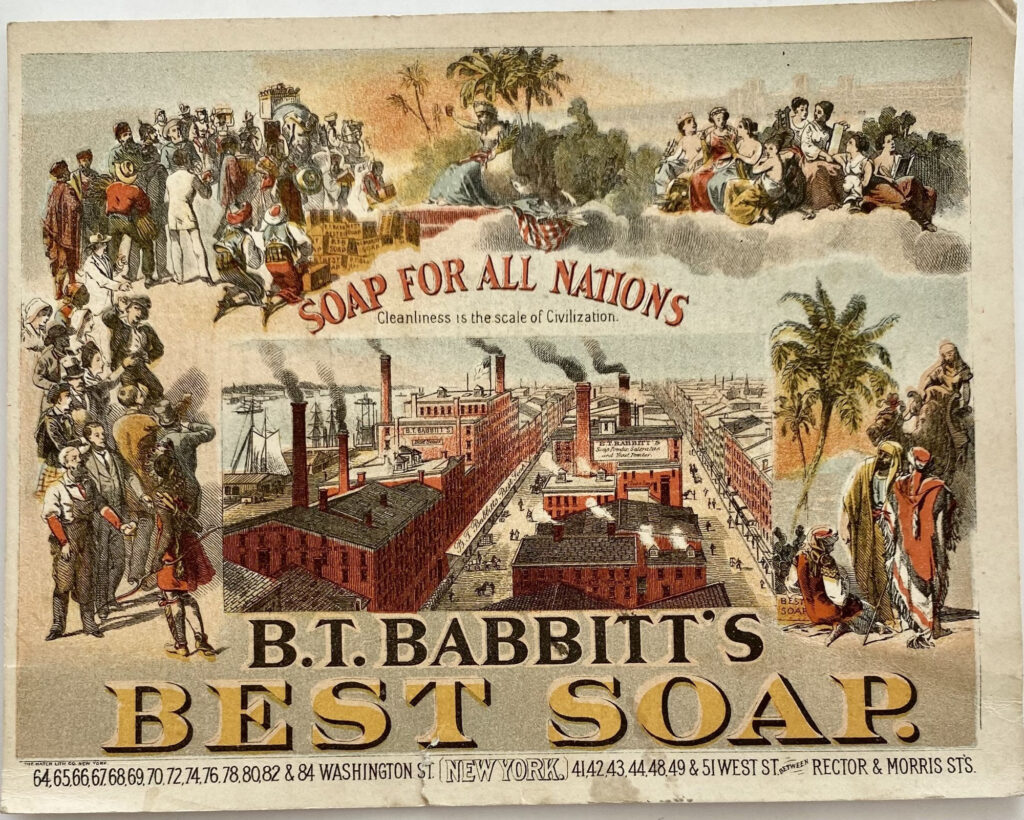

Well, we can thank one legendary man for the joy of free samples— Mr. Benjamin Babbitt!

Babbitt was quite the entrepreneur, owning a soap company that made a product called Babbitt’s Best Soap.

Babbitt was looking for ways to get more people to buy his soap. He had a bright idea: why not let people try it for free first?

In 1889, Babbitt put his idea into action. He hired teams to go door-to-door in cities handing out free trial-sized bars of his soap. Genius, right?

This way, people could test out the soap before deciding whether to buy it.

More than 10 million free soap samples were delivered over just 10 months!

The marketing tactic worked like a charm. Once folks tried out Babbitt’s soap, sales skyrocketed.

Babbitt had discovered the power of free samples. By letting people experience a product risk-free, they were more likely to go on to purchase it.

The concept caught on like wildfire. Soon, all sorts of companies were handing out free samples – food brands, medicine companies, you name it. They had caught on to Babbitt’s strategy for turning an unfamiliar product into a best-seller.

Nowadays, free samples are everywhere. From MamaEarth giving out free skincare samples to conditioner samples in magazines, Babbitt’s marketing innovation is still going strong.

So next time you’re munching on a free sample or trying out a new product for free, thank Babbitt for pioneering the idea!

#AskFinshots

This week’s question comes from Suraj Singhal from IIM Rohtak. Suraj asked—

“I have understood the different parameters to select the mutual fund but what are the different indicators or signs that one must look for to exit or redeem? What would be the optimal time frame to check if the fund is underperforming its benchmark?”

Hey Suraj, generally one year of underperformance should be a hint for you to look at what’s going on with your mutual fund investment.

For instance, the fund manager of the fund you’ve put your money in may have changed. If that’s the case it’s possible that the new manager is using a different fund management strategy. They could even change the assets the mutual fund invests in, which could lead to some changes in the way your investment performs.

But that doesn’t mean that you panic and hastily exit the fund. You could simply look at something called the portfolio turnover ratio which indicates the frequency with which fund managers bought or sold the assets under your fund over a period of time.

If this ratio is high, it could mean that fund managers are frequently churning the assets under your fund. And sometimes it could even be because of volatile market conditions. So don’t forget to look for that. Either way it could increase fund management costs, which could affect your returns.

Now, it may be hard for people outside of the wealth management industry to get access to all of this information quickly and react to changes. So the better option you could go with is choosing passively managed funds or what you call an index fund.

These funds simply mirror the performance of an index by holding the same or similar securities in the same proportions. Securities under these funds are only bought and sold when required to go hand in hand with an index. That can reduce the anxiety about how your investment is performing.

But remember, Finshots’ content is only for informational purposes. Please don’t take it as the gospel truth for financial advice. Always consult a financial expert.

Have a question for us at Finshots & Ditto?

Write to us at colleges@joinditto.in. And we’ll get our founders/experts to answer!

And that’s all for today folks! If you learned something new, make sure to subscribe to Finshots for more such insights 🙂

Finshots is now on WhatsApp Channels. Click here to follow us and get your daily financial fix in just 3 minutes.

Finshots is now on WhatsApp Channels. Click here to follow us and get your daily financial fix in just 3 minutes.