Micro, Small and Medium Enterprises form a vital component of the Indian economy, contributing to almost 29% of the GDP and roughly 40% to the export sector while generating the second-highest employment to about 45% of people in India. With approximately 50% of the MSMEs existing in the rural regions, it is evident that MSMEs are intertwined with the country’s rural economy. The expansion of this sector is necessary to deal with the economic disparity between the urban and rural areas and achieve the 5 trillion dollar economy as aimed by the current government.

The Definition

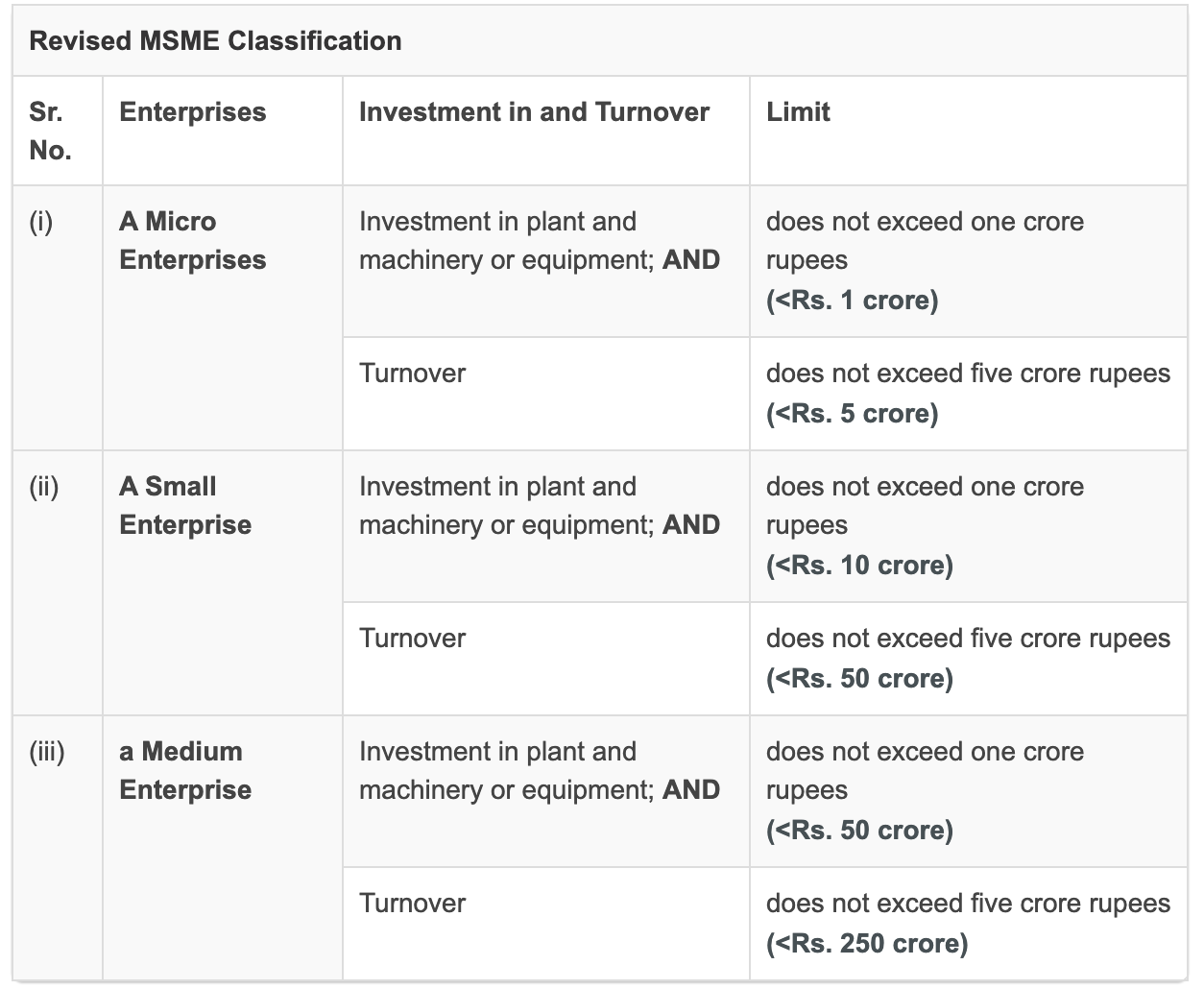

There are no universal criteria for small businesses; the definition varies from country to country. Some countries use the number of employers as a method of defining it but in India, the Micro, Small and Medium Enterprises Development Act (MSMED) of 2006 defines MSMEs based on the investment of equipment and the turnover.

The Status Quo

The pandemic has become one of the biggest hurdles when it comes to expanding this sector: Times of India surveys reported that Micro and Small industries saw revenue fall by 40-50%. The sector has also faced labour shortages and a significant crunch in liquidity and supply, because of which it is struggling to pay back its dues. Further, there is a lack of data on MSMEs; Federation of Indian MSME Secretary General Anil Bhardwaj said: “As per the economic census, there are about 63 million self-employed persons in India whereas, on the Udyam portal, only 2 million MSMEs are registered. There is a wedge of 61 million MSMEs since many people don’t want to get engaged into tax and other compliance issues that come with registration. With such a massive gap, obviously, it is difficult to know how many might have closed down.”

The survival of MSMEs depends on their access to working capital in the short term, and this liquidity injection cannot be left for banks to deal with. To begin with, there are numerous organisational and technical limitations. Financial institutions treat MSMEs as a single, standardised pool based on their turnover, which is not adequate to determine access to the working capital. It is possible to help understand their risk profiles and who they get funds from by decoding whom MSMEs purchase from and who they sell to:

- Category 1: MSMEs who are suppliers to larger Corporates or Government

- Category 2: MSMEs who purchase from larger Corporations and sell to retailers

- Category 3: MSMEs who directly sell their goods or services to end-customers

Access to working capital should be assessed based on real-time cash-flow, a popular concept in which financial technology comes into play. The implementation of GST has already established such financial technology by allowing users to input their cash flows (currently, it is not mandatory) and financial institutions could then use this data to give out loans rather than using collateral to determine credit.

Revival Measures and the Budget

The government launched various revival measures, out of which six were purely targeted towards MSMEs. These included

1. A definition-level change in MSMEs

2. The Credit and Finance Scheme (introduction of various schemes such as micro-credit scheme, Credit Guarantee scheme, Credit Guarantee Fund Trust For Micro And Small Enterprises and many more to provide funding assistance to financial institutions

3. Allocation of the ‘Fund of Funds’ for Equity Participation (strategy of asset allocation to redistribute their burden of risk and to enhance their scope of earnings)

4. Relief in Non-Performing Assets,

5. Clearing-off of dues to MSMEs

6. Disallowing Global Tenders to protect the MSMEs from the global competition as some of them are too weak to compete during a crisis brought upon by COVID-19

The budget made several provisions in various fields to induce growth in the sector. These include doubling the allocated resources to Rs. 15,700 crore from Rs. 7,572 crore, a Rs 20,000 crore subordinated debt for MSMEs, Rs 3 lakh crore collateral-free automatic loans for business, including MSMEs, and Rs 50,000 crore equity infusion through an ‘MSME Fund of Funds’. Apart from the monetary relief, the government has also aimed at honing the skills of the labour sector through a realignment of the National Apprenticeship Training Scheme (NATS) which provides post-education apprenticeship, training of graduates, and diploma holders in Engineering.

The nationwide lock-down initiation without any warning gave a significant blow to small industries besides revealing the country’s digital divide. Businesses in metro cities that were able to transition to online stores saw an increase in sales of up to 50%. Such transition required skilled labour and a consumer market with access to the technology, both of which are lacking in the country’s rural regions.

Union Minister Nitin Gadkari welcomed the announcements in the 2021 budget for MSMEs and said his ministry has planned to increase the sector’s contribution from 29 per cent to 50 per cent of the country’s GDP over the next five years and provide employment for 15 crore people. MSMEs hold great potential to expand the Indian economy and deal with poverty and unemployment issues, which plague the country.

Conclusion

It is evident that accomplishing economic growth and equity cannot be achieved without the expansion of MSMEs. The government must intervene and provide access to the working capital. This responsibility cannot be left to the banks alone as the livelihood of millions depend on this sector. With the formulation of correct policies and proper investment in this sector’s human resources, India can aspire to achieve an economy capable of surviving the future damages of any crisis it may face.